## Preamble: A Prelude to Understanding Auto Insurance Post-Accident

In the aftermath of a car accident, the journey towards recovery and resolution can be both physically and financially demanding. As you navigate the complexities of insurance claims, repair estimates, and medical expenses, it becomes paramount to understand the role of your auto insurance policy in mitigating the financial burden. This comprehensive guide will delve into the intricacies of auto insurance after an accident, empowering you with the knowledge to maximize coverage, navigate claims, and safeguard your financial well-being.

## Introduction: Unraveling the Significance of Auto Insurance

1.

Contents

- 1 The Foundation of Auto Insurance: A Safety Net for Unexpected Events

- 2 Navigating the Maze of Coverage Options: Understanding Your Policy

- 3 The Significance of Collision Coverage and Comprehensive Coverage

- 4 Understanding Deductibles: Your Financial Responsibility Threshold

- 5 The Claims Process: A Step-by-Step Guide

- 6 Maximizing Your Claim: Tips for Effective Communication

- 7 Challenging a Denied Claim: Asserting Your Rights

- 8 The Benefits of Auto Insurance: A Safety Net in Times of Need

- 9 Drawbacks of Auto Insurance: Understanding the Limitations

- 10 Exploring Exclusions: Situations Where Coverage May Not Apply

- 11 Assessing the Value of Uninsured/Underinsured Motorist Coverage

- 12 The Importance of Maintaining Continuous Coverage: Avoiding Lapses

- 13 The Role of SR-22 Insurance: Proof of Financial Responsibility

- 14 Understanding the Impact of At-Fault Accidents on Insurance Rates

- 15 Q: What should I do immediately after an accident?

- 16 Q: How long do I have to report an accident to my insurance company?

- 17 Q: What information do I need to provide when filing a claim?

- 18 Q: What happens if the other driver is uninsured or underinsured?

- 19 Q: What should I do if my insurance claim is denied?

- 20 Q: How can I lower my auto insurance premiums?

- 21 Q: What is SR-22 insurance

- 22 Share this:

- 23 Related posts:

The Foundation of Auto Insurance: A Safety Net for Unexpected Events

Auto insurance serves as a cornerstone of financial protection in the event of a car accident. By insuring your vehicle, you enter into a contract with an insurance company, which agrees to cover specific expenses related to damages and injuries incurred in an accident.

2.

Auto insurance policies vary in their coverage limits and provisions. It is essential to meticulously review your policy to grasp the extent of coverage you have for different types of accidents and expenses, including property damage, bodily injury, and medical payments.

3.

The Significance of Collision Coverage and Comprehensive Coverage

Collision coverage specifically caters to damages sustained by your own vehicle in an accident, regardless of fault. Comprehensive coverage, on the other hand, extends protection to your vehicle against non-collision-related events such as theft, vandalism, and natural disasters.

4.

Understanding Deductibles: Your Financial Responsibility Threshold

Deductibles represent the amount you agree to pay out-of-pocket before your insurance coverage kicks in. Selecting a higher deductible typically results in lower insurance premiums, while a lower deductible provides more immediate financial assistance in the event of an accident.

5.

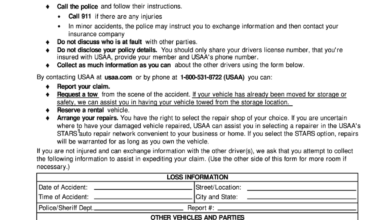

The Claims Process: A Step-by-Step Guide

In the aftermath of an accident, promptly reporting the incident to your insurance company is paramount. The claims process typically involves filing a claim, providing documentation of the accident, and cooperating with the insurance adjuster to determine the extent of damages and liability.

6.

Maximizing Your Claim: Tips for Effective Communication

Clear and consistent communication is crucial throughout the claims process. Keep a detailed record of all expenses related to the accident, including medical bills, repair estimates, and lost wages. Be prepared to provide thorough information to the insurance adjuster to ensure a fair and timely settlement.

7.

Challenging a Denied Claim: Asserting Your Rights

If your insurance claim is denied, it is important to understand your rights and options. Review your policy carefully to identify any potential grounds for appeal. Consider seeking legal advice or contacting your state’s insurance regulatory agency for guidance on disputing the denial.

## Strengths and Weaknesses: Weighing the Pros and Cons of Auto Insurance

1.

The Benefits of Auto Insurance: A Safety Net in Times of Need

Auto insurance provides invaluable protection against the financial consequences of an accident, offering peace of mind and safeguarding your assets. It covers expenses such as medical bills, vehicle repairs, and legal fees, mitigating the burden on your personal finances.

2.

Drawbacks of Auto Insurance: Understanding the Limitations

While auto insurance offers significant benefits, it also has limitations. Coverage limits may not always be sufficient to cover all expenses, and deductibles can impose financial responsibility. Additionally, insurance premiums can be a significant financial obligation, especially for high-risk drivers or those with poor driving records.

3.

Exploring Exclusions: Situations Where Coverage May Not Apply

Auto insurance policies typically include exclusions that limit coverage under certain circumstances, such as driving under the influence of alcohol or drugs, participating in illegal activities, or using your vehicle for commercial purposes. It is crucial to be aware of these exclusions to avoid unexpected financial liability.

4.

Assessing the Value of Uninsured/Underinsured Motorist Coverage

Uninsured/underinsured motorist coverage provides protection in the event of an accident with a driver who is uninsured or underinsured. This coverage is particularly valuable in states with high rates of uninsured motorists, as it ensures that you have access to compensation for your injuries and damages.

5.

The Importance of Maintaining Continuous Coverage: Avoiding Lapses

Maintaining continuous auto insurance coverage is essential to avoid gaps in protection and potential penalties. Lapses in coverage can lead to higher premiums and create barriers to obtaining insurance in the future. It is advisable to set up automatic payments or reminders to ensure timely premium payments.

6.

The Role of SR-22 Insurance: Proof of Financial Responsibility

In some cases, drivers may be required to obtain an SR-22 insurance certificate as proof of financial responsibility. This requirement typically arises after a serious traffic violation, such as driving under the influence of alcohol or drugs, or after multiple traffic citations.

7.

Understanding the Impact of At-Fault Accidents on Insurance Rates

If you are found to be at fault for an accident, your insurance company may adjust your premiums accordingly. The extent of the rate increase will vary depending on factors such as the severity of the accident, your driving history, and the state in which you reside.

## Comprehensive Table: A Summary of Auto Insurance After Accident

| **Coverage Type** | **Description** | **Benefits** | **Drawbacks** |

|—|—|—|—|

| **Collision Coverage** | Covers damage to your own vehicle in an accident | Provides financial assistance for vehicle repairs or replacement | May have a high deductible |

| **Comprehensive Coverage** | Protects your vehicle from non-collision events, such as theft and vandalism | Offers peace of mind and comprehensive protection | Typically has a higher premium than collision coverage |

| **Bodily Injury Liability Coverage** | Covers injuries sustained by others in an accident you cause | Protects you from financial liability for medical expenses and lost wages | Liability limits may not be sufficient to fully cover damages |

| **Property Damage Liability Coverage** | Pays for damage to property belonging to others in an accident you cause | Protects you from financial liability for repairs or replacement | Liability limits may not be sufficient to fully cover damages |

| **Medical Payments Coverage** | Covers medical expenses for you and your passengers, regardless of fault | Offers immediate financial assistance for medical bills | May have a low coverage limit |

| **Uninsured/Underinsured Motorist Coverage** | Provides protection in the event of an accident with an uninsured or underinsured driver | Ensures you have access to compensation for your injuries and damages | May have a higher premium |

| **SR-22 Insurance** | Proof of financial responsibility required after certain traffic violations | Allows you to maintain driving privileges | Typically has a higher premium |

## FAQs: Clarifying Common Inquiries

1.

Q: What should I do immediately after an accident?

A: After an accident, it is crucial to remain calm and take the following steps: Ensure the safety of yourself and others, call 911 to report the accident, exchange information with the other driver(s) involved, take photos of the damage, and contact your insurance company promptly.

2.

Q: How long do I have to report an accident to my insurance company?

A: You should report the accident to your insurance company as soon as possible. Most states have a time limit for reporting accidents, typically ranging from 24 hours to 30 days.

3.

Q: What information do I need to provide when filing a claim?

A: When filing a claim, you will typically need to provide your insurance policy number, the date and location of the accident, a description of the accident, the names and contact information of the other driver(s) involved, and any witnesses.

4.

Q: What happens if the other driver is uninsured or underinsured?

A: If the other driver is uninsured or underinsured, you may be able to file a claim under your own uninsured/underinsured motorist coverage. However, this coverage may have limits, and it is important to understand the details of your policy.

5.

Q: What should I do if my insurance claim is denied?

A: If your insurance claim is denied, you should review your policy carefully to identify any potential grounds for appeal. You may also consider seeking legal advice or contacting your state’s insurance regulatory agency for guidance.

6.

A: There are several ways to potentially lower your auto insurance premiums, such as maintaining a good driving record, taking defensive driving courses, bundling your insurance policies, and increasing your deductible.

7.

{kind=link}