Contents

- 1 A Preamble to Insurance Policy Transformation

- 2 1. Understanding the Potential Benefits of Switching Auto Insurance After Accident

- 3 2. Considering the Potential Drawbacks of Switching Auto Insurance After Accident

- 4 3. Weighing the Strengths and Weaknesses

- 5 4. Determining the Right Time to Switch Auto Insurance After Accident

- 6 5. Shopping for a New Auto Insurance Policy After Accident

- 7 6. Making the Switch

- 8 7. Frequently Asked Questions (FAQs)

- 8.1 7.1 How long should I wait to switch auto insurance after an accident?

- 8.2 7.2 Will my premiums increase if I switch auto insurance after an accident?

- 8.3 7.3 What are the benefits of switching auto insurance after an accident?

- 8.4 7.4 What are the risks of switching auto insurance after an accident?

- 8.5 7.5 How do I find the best auto insurance policy after an accident?

- 8.6 7.6 What should I do if I am not satisfied with my new auto insurance policy?

- 8.7 7.7 Can I switch auto insurance providers if I am still paying off my car?

- 8.8 7.8 What happens to my uninsured motorist coverage if I switch auto insurance providers?

- 8.9 7.9 Can I switch auto insurance providers if I have an SR-22?

- 8.10 7.10 What is a grace period for auto insurance?

- 8.11 7.11 Can I cancel my auto insurance policy at any time?

- 8.12 7.12 What happens if I am in an accident and I do not have auto insurance?

- 8.13 7.13 How can I get affordable auto insurance?

- 8.14 Share this:

- 8.15 Related posts:

A Preamble to Insurance Policy Transformation

In the aftermath of an automotive collision, navigating the complexities of insurance can be a daunting task. One crucial decision that arises is whether to switch auto insurance providers. This guide will delve into the intricacies of this decision, exploring the potential benefits and considerations associated with switching auto insurance after an accident.

The decision to switch auto insurance after an accident is influenced by a myriad of factors, including the severity of the accident, the fault assignment, and the policy provisions of the current insurer. Understanding the implications of each of these elements is paramount in making an informed choice.

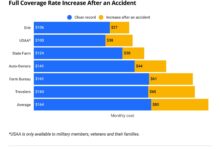

Insurance companies assess risk based on a multitude of factors, and an accident can significantly alter this assessment. If you are deemed at fault for the accident, your insurance premiums are likely to increase, as insurers view you as a higher-risk driver. The extent of the premium increase will vary depending on the insurance company’s underwriting guidelines and the severity of the accident.

In contrast, if you are not deemed at fault for the accident, you may still consider switching auto insurance providers. Your current insurer may not offer the best coverage options or rates for your specific needs. Exploring alternative providers can help you secure more comprehensive coverage at a more competitive premium.

1. Understanding the Potential Benefits of Switching Auto Insurance After Accident

1.1 Lower Premiums for Not-at-Fault Drivers

Insurance companies reward safe driving habits. If you have a clean driving record and are not at fault for the accident, shopping for a new insurance provider can yield significant savings. By switching to a company that recognizes your responsible driving history, you may qualify for lower premiums.

1.2 Enhanced Coverage Options

Not all insurance companies offer the same level of coverage. After an accident, you may realize that your current policy does not provide adequate protection. Switching to a provider that offers more comprehensive coverage can give you peace of mind and ensure that you are fully protected in the event of future accidents.

1.3 Improved Customer Service

Customer service plays a crucial role in the insurance experience. If you have experienced unsatisfactory service from your current insurer, switching providers can provide an opportunity to find a company that values customer satisfaction and provides prompt assistance when you need it most.

2. Considering the Potential Drawbacks of Switching Auto Insurance After Accident

2.1 Potential Premium Increases for At-Fault Drivers

If you are deemed at fault for the accident, switching auto insurance providers may not yield lower premiums. Insurance companies typically charge higher premiums for drivers with recent at-fault accidents, regardless of the previous insurer.

2.2 Loss of Claim History

When you switch insurance companies, you typically lose your claim history with your previous insurer. This can be a disadvantage if you have filed multiple claims in the past, as your new insurer may view you as a high-risk driver and charge higher premiums accordingly.

2.3 Cancellation Fees and Coverage Gaps

Canceling your current auto insurance policy before the expiration date may result in cancellation fees. Additionally, there is a risk of experiencing a coverage gap if there is a delay in securing a new policy.

3. Weighing the Strengths and Weaknesses

The decision to switch auto insurance after an accident requires careful consideration of both the potential benefits and drawbacks. Here is a tabular summary of the key factors to consider:

| Factor | Strength | Weakness |

|---|---|---|

| Premium Cost | Lower premiums for not-at-fault drivers | Higher premiums for at-fault drivers |

| Coverage Options | Improved coverage options | Potential loss of certain coverages |

| Customer Service | Improved customer service | Unknown quality of customer service with new insurer |

| Claim History | N/A | Loss of claim history |

| Cancellation Fees | N/A | Potential cancellation fees |

| Coverage Gaps | N/A | Risk of coverage gap |

4. Determining the Right Time to Switch Auto Insurance After Accident

There is no one-size-fits-all answer to the question of when to switch auto insurance after an accident. However, there are certain situations that may warrant a switch:

- You are not at fault for the accident and your current premiums have increased significantly.

- You are not satisfied with the coverage options or customer service provided by your current insurer.

- You have found a new insurer that offers more comprehensive coverage at a lower cost.

5. Shopping for a New Auto Insurance Policy After Accident

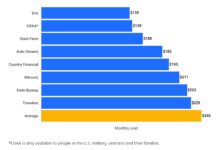

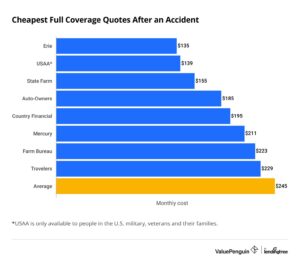

If you decide to switch auto insurance providers after an accident, it is important to shop around and compare quotes from multiple companies. Here are some tips for finding the best policy:

- Gather information about your driving history, vehicle, and coverage needs.

- Obtain quotes from at least three different insurance companies.

- Compare the coverage options, deductibles, and premiums offered by each company.

- Read the policy documents carefully before making a final decision.

6. Making the Switch

Once you have chosen a new auto insurance provider, you can begin the process of switching policies. Here are the steps to follow:

- Contact your new insurer and provide them with the necessary information.

- Cancel your current policy and pay any outstanding premiums or cancellation fees.

- Provide proof of insurance to your lender or leasing company, if applicable.

- Review your new policy carefully to ensure that you understand the coverage and limits.

7. Frequently Asked Questions (FAQs)

7.1 How long should I wait to switch auto insurance after an accident?

There is no set waiting period to switch auto insurance after an accident. However, it is advisable to wait until your claim has been settled and any fault determinations have been made.

The impact on your premiums will depend on whether you are at fault for the accident and the underwriting guidelines of the new insurer.

7.3 What are the benefits of switching auto insurance after an accident?

Potential benefits include lower premiums for not-at-fault drivers, enhanced coverage options, and improved customer service.

7.4 What are the risks of switching auto insurance after an accident?

Potential risks include higher premiums for at-fault drivers, loss of claim history, and cancellation fees.

7.5 How do I find the best auto insurance policy after an accident?

Shop around and compare quotes from multiple insurance companies to find the best coverage and rates.

7.6 What should I do if I am not satisfied with my new auto insurance policy?

If you are not satisfied with your new policy, you can contact the insurer to discuss your concerns or consider switching providers again.

7.7 Can I switch auto insurance providers if I am still paying off my car?

Yes, you can switch auto insurance providers even if you are still paying off your car. However, you will need to provide proof of insurance to your lender or leasing company.

7.8 What happens to my uninsured motorist coverage if I switch auto insurance providers?

Your uninsured motorist coverage will transfer to your new auto insurance policy. However, you should review your new policy to ensure that the coverage limits are adequate.

7.9 Can I switch auto insurance providers if I have an SR-22?

Yes, you can switch auto insurance providers if you have an SR-22. However, you will need to find an insurer that is willing to accept drivers with SR-22s.

7.10 What is a grace period for auto insurance?

A grace period for auto insurance is a short period of time after your policy expires in which you can renew your policy without penalty.

7.11 Can I cancel my auto insurance policy at any time?

Yes, you can cancel your auto insurance policy at any time. However, you may be subject to cancellation fees.

7.12 What happens if I am in an accident and I do not have auto insurance?

If you are in an accident and you do not have auto insurance, you may be held financially responsible for the damages. You may also face legal penalties.

7.13 How can I get affordable auto insurance?

There are a number of ways to get

{kind=link}