Contents

- 1 Introduction

- 2 Understanding Your Coverage

- 3 Filing a Claim

- 4 Determining Fault

- 5 Navigating the Claims Process

- 6 Potential Consequences for Your Insurance

- 7 Protecting Your Rights

- 8 Planning for the Future

- 9 Conclusion

- 10 Call to Action

- 11 Closing Words

- 12 FAQs

- 12.1 Q: What should I do immediately after an accident?

- 12.2 Q: How do I determine fault for an accident?

- 12.3 Q: What are the potential consequences of filing a claim for an accident?

- 12.4 Q: What should I do if I disagree with my insurance company’s assessment of fault?

- 12.5 Q: How can I keep my insurance costs low after an accident?

- 12.6 Q: What should I do if I am uninsured or underinsured at the time of an accident?

- 12.7 Share this:

- 12.8 Related posts:

Introduction

Navigating the aftermath of an automobile accident can be a daunting task. One of the most pressing concerns is the impact on your auto insurance. Understanding how car insurance works after an accident can help you protect your financial interests and ensure a smooth claims process.

This comprehensive guide will provide you with everything you need to know about auto insurance after an accident, including the following key aspects:

- Understanding your coverage

- Filing a claim

- Determining fault

- Navigating the claims process

- Potential consequences for your insurance

- Protecting your rights

- Planning for the future

Understanding Your Coverage

Types of Auto Insurance

The coverage you have will play a significant role in how your claim is handled. Common types of auto insurance include:

- Liability coverage: Covers damages caused to other parties in an accident you are at fault for.

- Collision coverage: Covers damages to your own vehicle, regardless of fault.

- Comprehensive coverage: Covers damages caused by factors other than a collision, such as theft or vandalism.

- Uninsured/underinsured motorist coverage: Covers damages caused by drivers who do not have adequate insurance.

Coverage Limits

It is essential to understand the coverage limits of your policy. These limits determine the maximum amount your insurance company will pay for damages. You can typically adjust your coverage limits to suit your needs and financial situation.

Filing a Claim

Reporting the Accident

After an accident, it is crucial to report it to your insurance company promptly. Most policies require you to report the accident within a specified timeframe, usually within a few days. Failure to do so could affect your claim.

Gather Evidence

To support your claim, gather as much evidence as possible, including:

- Police report (if applicable)

- Photos of the damage

- Witness statements

- Medical records (if there were injuries)

Determining Fault

Fault Laws

Determining who is at fault for an accident is crucial for insurance purposes. There are two main types of fault laws:

- Contributory negligence: If you are at all at fault for the accident, you cannot recover any damages from the other party.

- Comparative negligence: You can recover damages from the other party even if you are partially at fault, but the amount you recover will be reduced by your percentage of fault.

Evidence of Fault

To establish fault, insurance companies will consider evidence such as:

- Police report

- Witness statements

- Photos and videos of the scene

- Medical records

- Traffic camera footage

Adjusters and Appraisals

Insurance companies typically assign adjusters to handle claims. Adjusters will investigate the accident, assess the damages, and make a settlement offer. If you are not satisfied with the offer, you can request an appraisal, which involves an independent adjuster reviewing the case.

Settlement Negotiations

Once the damages have been assessed, you will negotiate a settlement with the insurance company. It is important to understand the value of your claim and be prepared to negotiate on your behalf.

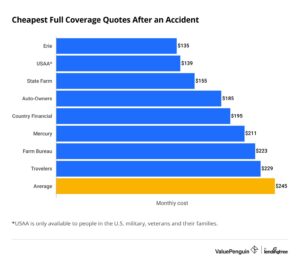

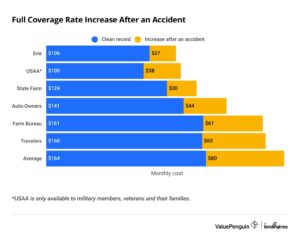

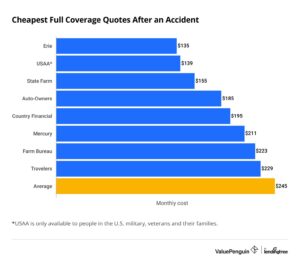

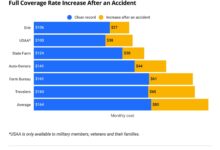

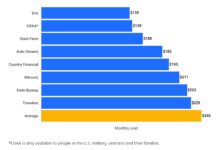

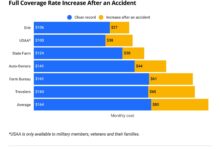

Potential Consequences for Your Insurance

Rate Increases

Filing a claim can lead to an increase in your insurance rates. However, the severity of the accident and your driving history will also affect the extent of the increase.

Loss of Coverage

In some cases, a claim can result in the loss of coverage if the insurance company deems you are too high-risk. This is especially true for repeat claims or accidents that involve serious injuries or property damage.

Protecting Your Rights

Hiring an Attorney

If you have a complex claim or if the insurance company is disputing your case, you may consider hiring an attorney. An attorney can protect your rights and negotiate on your behalf.

Filing a Complaint

If you are not satisfied with the way your claim is being handled, you can file a complaint with your state’s insurance regulator. This can help resolve disputes and ensure fair treatment.

Planning for the Future

Increasing Coverage

After an accident, you may want to consider increasing your coverage to provide better protection in the future. This can help reduce the financial impact of any future accidents.

Maintaining a Good Driving Record

Maintaining a clean driving record is the best way to keep your insurance rates low. Avoid traffic violations and accidents to keep your insurance costs under control.

Conclusion

Understanding the intricacies of auto insurance after an accident can empower you to navigate the claims process confidently and protect your financial interests. Remember, the most important thing is to ensure your safety and well-being following an accident. By working closely with your insurance company and being prepared, you can minimize the stress and maximize the benefits of your coverage.

Call to Action

Don’t wait until after an accident to understand your auto insurance coverage. Review your policy regularly and make any necessary adjustments to ensure you have adequate protection. If you have any questions or concerns, contact your insurance company or an insurance agent for assistance. By being proactive and informed, you can safeguard your financial未来 and provide peace of mind for yourself and your loved ones.

Closing Words

As you navigate the aftermath of an automobile accident, it is essential to remember that you are not alone. Your insurance company is there to provide support and guidance throughout the claims process. By understanding your rights, protecting your interests, and planning for the future, you can recover from this challenging experience with confidence and resilience.

| Aspect | Description |

|---|---|

| Types of Coverage | Liability, collision, comprehensive, uninsured/underinsured motorist |

| Coverage Limits | Determine the maximum amount your insurance company will pay for damages |

| Reporting the Accident | Notify your insurance company promptly within the specified timeframe |

| Fault Laws | Contributory negligence or comparative negligence laws determine fault and recovery |

| Evidence of Fault | Gather evidence such as police reports, witness statements, and photos |

| Rate Increases | Filing a claim can lead to higher insurance rates, depending on the severity and your driving history |

| Loss of Coverage | Repeat claims or serious accidents may result in the loss of insurance coverage |

| Hiring an Attorney | Consider legal representation for complex claims or disputes with the insurance company |

| Filing a Complaint | Resolve disputes by filing a complaint with your state’s insurance regulator |

| Increasing Coverage | Adjust your coverage limits to provide better protection in the future |

| Maintaining a Good Driving Record | Avoid traffic violations and accidents to keep insurance costs low |

FAQs

Q: What should I do immediately after an accident?

A: Ensure safety, call 911 if necessary, exchange information with the other driver, and report the accident to your insurance company promptly.

Q: How do I determine fault for an accident?

A: Insurance companies will consider evidence such as police reports, witness statements, and photos to establish fault.

Q: What are the potential consequences of filing a claim for an accident?

A: Filing a claim can lead to increased insurance rates or even loss of coverage if the insurance company deems you are too high-risk.

Q: What should I do if I disagree with my insurance company’s assessment of fault?

A: Request an appraisal, file a complaint with your state’s insurance regulator, or consider hiring an attorney to protect your rights.

Q: How can I keep my insurance costs low after an accident?

A: Maintain a good driving record by avoiding traffic violations and accidents.

Q: What should I do if I am uninsured or underinsured at the time of an accident?

A: Contact the other driver’s insurance