Contents

- 1 Auto Insurance For Accidents

- 1.1 An In-Depth Analysis and Comprehensive Guide

- 1.2 The Importance of Auto Insurance for Accidents

- 1.3 Strengths of Auto Insurance for Accidents

- 1.4 Weaknesses of Auto Insurance for Accidents

- 1.5 Types of Auto Insurance Coverage for Accidents

- 1.6 Determining the Right Auto Insurance Coverage for Accidents

- 1.7 Cost of Auto Insurance for Accidents

- 1.8 Filing a Claim for Auto Insurance for Accidents

- 1.9 Conclusion

- 1.10 FAQs about Auto Insurance for Accidents

Auto Insurance For Accidents

An In-Depth Analysis and Comprehensive Guide

The realm of auto insurance is a complex web of policies and regulations that can often leave individuals feeling bewildered and uncertain. However, understanding the intricacies of this protection is paramount for securing financial stability and peace of mind in the event of an accident. This article delves into the depths of auto insurance for accidents, exploring its strengths, weaknesses, and indispensable value in safeguarding drivers against the unforeseen.

Auto insurance for accidents serves as a financial safety net, providing a buffer against the potentially devastating costs associated with vehicular collisions. When an accident occurs, insurance coverage can alleviate the burden of medical expenses, vehicle repairs, and other related costs, ensuring that individuals can focus on recovery and rebuilding their lives.

However, auto insurance is not without its complexities. Comprehending the various coverage options, deductibles, and exclusions is essential for tailoring a policy that meets individual needs and circumstances. Failure to do so may result in inadequate protection or unexpected financial liabilities in the aftermath of an accident.

Navigating the landscape of auto insurance for accidents requires a multifaceted approach. This article unravels the complexities of this vital protection, empowering individuals to make informed decisions and safeguard themselves against the financial repercussions of accidents.

The Importance of Auto Insurance for Accidents

The significance of auto insurance for accidents cannot be overstated. In the United States alone, motor vehicle crashes account for thousands of fatalities and millions of injuries each year. The financial impact of these accidents can be staggering, with medical bills, property damage, and lost wages often reaching astronomical figures.

Auto insurance for accidents provides a crucial safety net, protecting individuals from the financial devastation that can accompany a collision. By covering the costs of medical expenses, vehicle repairs, and other related expenses, insurance helps to ensure that individuals can focus on their physical and emotional recovery without the added burden of financial stress.

Moreover, auto insurance for accidents plays a vital role in protecting other drivers and pedestrians. By ensuring that at-fault drivers are financially responsible for the damages they cause, insurance helps to reduce the likelihood of individuals being left with unpaid medical bills or property damage.

Strengths of Auto Insurance for Accidents

Auto insurance for accidents offers a multitude of strengths that make it an indispensable form of protection for drivers. These strengths include:

Financial Security:

In the event of an accident, auto insurance provides a financial safety net, ensuring that individuals are not left with overwhelming medical expenses, vehicle repair costs, or other related expenses. This financial security allows individuals to focus on their recovery and rebuilding their lives, without the added burden of financial stress.

Peace of Mind:

Knowing that they are financially protected in the event of an accident provides drivers with peace of mind. This peace of mind allows them to drive with confidence, knowing that they are not solely responsible for the financial consequences of an accident.

Legal Protection:

Auto insurance for accidents provides legal protection for drivers in the event of a lawsuit. If an at-fault driver is sued for damages, their insurance policy will provide coverage for legal fees and any damages that are awarded to the plaintiff.

Weaknesses of Auto Insurance for Accidents

While auto insurance for accidents offers significant strengths, it is not without its weaknesses. These weaknesses include:

Policy Limits:

Auto insurance policies have coverage limits, which can vary depending on the policyholder’s needs and financial circumstances. In some cases, the coverage limits may not be sufficient to cover all of the damages resulting from an accident, leaving the policyholder responsible for the remaining costs.

Deductibles:

Deductibles are the amount of money that the policyholder is responsible for paying out of pocket before their insurance coverage kicks in. Higher deductibles can result in lower insurance premiums, but they also mean that the policyholder will have to pay more out of pocket in the event of an accident.

Exclusions:

Auto insurance policies may contain exclusions that limit coverage for certain types of accidents or damages. For example, some policies may exclude coverage for accidents caused by drunk driving or racing.

Types of Auto Insurance Coverage for Accidents

There are various types of auto insurance coverage that can provide protection in the event of an accident. These types of coverage include:

Liability Coverage:

Liability coverage provides protection for bodily injury and property damage that is caused to others as a result of an accident. Liability coverage is required by law in most states.

Collision Coverage:

Collision coverage provides protection for damage to the policyholder’s own vehicle as a result of an accident. Collision coverage is not required by law, but it is highly recommended.

Comprehensive Coverage:

Comprehensive coverage provides protection for damage to the policyholder’s own vehicle as a result of non-collision events, such as theft, vandalism, or natural disasters. Comprehensive coverage is not required by law, but it is highly recommended.

Determining the Right Auto Insurance Coverage for Accidents

Determining the right auto insurance coverage for accidents depends on a number of factors, including the policyholder’s financial needs, driving history, and the value of their vehicle. The following steps can help policyholders determine the right coverage for their needs:

Assess Financial Needs:

Policyholders should first assess their financial needs in the event of an accident. This assessment should include consideration of medical expenses, vehicle repairs, and other related costs.

Review Driving History:

Policyholders should review their driving history to identify any factors that could affect their insurance premiums, such as traffic violations or accidents.

Determine Vehicle Value:

Policyholders should determine the value of their vehicle to ensure that they have adequate coverage in the event of an accident.

Cost of Auto Insurance for Accidents

The cost of auto insurance for accidents varies depending on a number of factors, including the policyholder’s age, gender, driving history, and the type of coverage selected. The following factors can affect the cost of auto insurance for accidents:

Age:

Younger drivers tend to pay higher insurance premiums than older drivers due to their lack of experience and higher risk of accidents.

Gender:

In some states, male drivers pay higher insurance premiums than female drivers due to statistical evidence that male drivers are more likely to be involved in accidents.

Driving History:

Drivers with a clean driving history tend to pay lower insurance premiums than drivers with a history of traffic violations or accidents.

Type of Coverage:

The type of coverage selected can also affect the cost of auto insurance. Liability-only coverage is typically the least expensive, while comprehensive coverage is the most expensive.

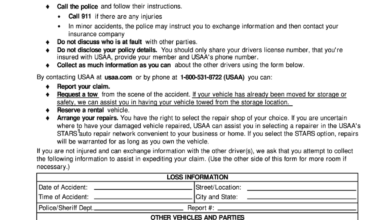

Filing a Claim for Auto Insurance for Accidents

In the event of an accident, policyholders should follow these steps to file a claim for auto insurance:

Contact Insurance Company:

Policyholders should contact their insurance company as soon as possible after an accident to report the claim.

Provide Information:

Policyholders should provide the insurance company with as much information as possible about the accident, including the date, time, location, and details of the accident.

Submit Documentation:

Policyholders may need to submit documentation to support their claim, such as a police report, medical records, and photos of the damage.

Conclusion

Auto insurance for accidents is a valuable form of protection that can provide financial security, peace of mind, and legal protection in the event of an accident. While it is not without its weaknesses, the strengths of auto insurance far outweigh the weaknesses, making it an indispensable form of protection for drivers.

By understanding the strengths, weaknesses, and types of auto insurance coverage available, policyholders can determine the right coverage for their needs and circumstances. In the event of an accident, policyholders should follow the steps outlined above to file a claim for auto insurance.

Auto insurance for accidents is an essential form of protection that every driver should have. By taking the time to understand the coverage options and the claims process, policyholders can ensure that they are financially protected in the event of an accident.

FAQs about Auto Insurance for Accidents

-

What is auto insurance for accidents?

Auto insurance for accidents is a type of insurance that provides financial protection to drivers in the event of an accident.

-

What are the benefits of auto insurance for accidents?

Auto insurance for accidents provides a number of benefits, including financial security, peace of mind, and legal protection.

-

What are the different types of auto insurance coverage for accidents?

There are three main types of auto insurance coverage for accidents: liability coverage, collision coverage, and comprehensive coverage.

-

How much does auto insurance for accidents cost?

The cost of auto insurance for accidents varies depending on a number of factors, including the policyholder’s age, gender, driving history, and the type of coverage selected.

Related posts:

{kind=link}