Contents

Introductory Words

Accidents happen, and when they do, it’s crucial to have auto insurance to protect yourself financially. However, drivers with accidents face unique challenges when obtaining insurance, as they are often perceived as higher-risk drivers. This article aims to provide comprehensive information about auto insurance for drivers with accidents, including the impact on premiums, coverage options, and available solutions.

Introduction

Auto insurance serves as a safety net, providing financial protection in the event of an accident. It covers costs such as medical expenses, property damage, and legal liability. However, for drivers with accidents, obtaining auto insurance can be more complex and expensive. Insurance companies assess risk based on various factors, and accidents are often viewed as indicators of increased risk. As a result, drivers with accidents may face higher premiums, diminished coverage options, or even denial of coverage.

Understanding the Impact of Accidents on Auto Insurance

Accidents significantly impact auto insurance rates. Insurance companies use claims history and accident data to determine the likelihood of future accidents. The severity of the accident, the extent of damages, and the driver’s fault play a crucial role in determining the premium increase.

Fault Determination

When determining fault in an accident, insurance companies rely on police reports and witness statements. The driver who is deemed at fault for the accident faces higher premiums as they are considered more likely to cause future accidents.

Accident Frequency

Multiple accidents within a short period can drastically increase premiums. Insurance companies view frequent accidents as a pattern of risky driving behavior, resulting in a higher risk assessment.

Accident Severity

The severity of an accident also affects premiums. Accidents involving injuries, property damage, or total loss typically result in higher premiums compared to minor fender benders.

Strengths and Weaknesses of Auto Insurance for Drivers with Accidents

**Strengths**

* Financial protection: Auto insurance provides coverage for medical expenses, property damage, and legal liability, even for drivers with accidents.

* Reduced financial stress: Insurance coverage reduces the financial burden associated with accident costs.

* Legal compliance: Most states require drivers to carry auto insurance.

**Weaknesses**

* Higher premiums: Drivers with accidents may face higher premiums due to increased risk assessment.

* Coverage restrictions: Insurance companies may limit coverage or exclude certain drivers based on accident history.

* Denial of coverage: In some cases, insurance companies may deny coverage to drivers with multiple or severe accidents.

Comprehensive Table: Auto Insurance for Drivers with Accidents

| Feature | Description |

|—|—|

| Availability | Accident history may affect availability and coverage options. |

| Coverage | Coverage may be limited or excluded for certain drivers. |

| Premium Costs | Premiums are typically higher for drivers with accidents. |

| High-Risk Policies | Special insurance policies designed for drivers with accidents. |

| Driver Monitoring Programs | Programs that monitor driver behavior and may offer premium discounts. |

FAQs

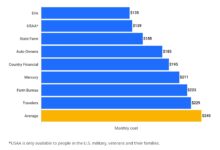

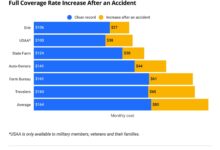

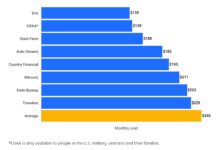

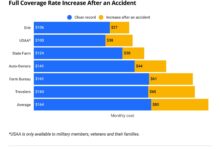

**Q1: How much do premiums increase after an accident?**

**A1:** Premium increases vary depending on the severity of the accident, fault determination, and the driver’s insurance history. Typically, premiums can increase by 20-50%.

**Q2: Can I get insurance if I have multiple accidents?**

**A2:** It depends on the insurance company and the circumstances. Drivers with multiple accidents may be required to obtain high-risk insurance policies or may face coverage restrictions.

**Q3: What is a high-risk insurance policy?**

**A3:** High-risk insurance policies are designed for drivers who fall into higher-risk categories, such as drivers with accidents or poor driving records. These policies typically have higher premiums but may provide limited coverage options.

**Q4: Can I lower my premiums after an accident?**

**A4:** Yes, premiums may be lowered over time if the driver maintains a clean driving record and demonstrates responsible driving behavior. Completing defensive driving courses or installing telematics devices may also help reduce premiums.

**Q5: What is a driver monitoring program?**

**A5:** Driver monitoring programs use telematics devices to track driving behavior, such as speed, braking, and acceleration. Participation in these programs can provide data-driven feedback and may qualify drivers for premium discounts.

**Q6: How long does an accident stay on my record?**

**A6:** Accidents typically remain on insurance records for 3-5 years. However, insurance companies may consider accidents up to 7 years or more in certain cases.

**Q7: Can I dispute an accident on my record?**

**A7:** Yes, drivers can dispute accidents on their records if they believe the information is inaccurate. Documentation and evidence to support the dispute should be provided to the insurance company.

**Q8: What happens if I get into another accident while I have a high-risk policy?**

**A8:** Getting into another accident while holding a high-risk policy can further increase premiums and may make it challenging to obtain future coverage. It is essential to maintain safe driving practices to avoid additional accidents.

**Q9: How can I improve my driving record?**

**A9:** Drivers can improve their driving records by maintaining a clean driving record, completing defensive driving courses, and participating in driver monitoring programs.

**Q10: What other factors affect my auto insurance premiums?**

**A10:** Other factors that affect premiums include age, driving experience, vehicle type, location, and coverage limits.

**Q11: Can I get car insurance without a driver’s license?**

**A11:** Typically, obtaining car insurance requires a valid driver’s license. However, some insurers may offer non-driver insurance policies for individuals who do not have a driver’s license or who have had their license suspended or revoked.

**Q12: What is uninsured motorist coverage?**

**A12:** Uninsured motorist coverage provides protection to drivers in the event of an accident caused by an uninsured or underinsured driver.

**Q13: Is it legal to drive without car insurance?**

**A13:** In most states, it is illegal to drive without car insurance. Drivers caught driving without insurance may face fines, penalties, or license suspension.

Conclusion

Obtaining auto insurance after an accident can present challenges, but it is crucial for protecting against financial liabilities. Understanding the impact of accidents on premiums and coverage options is essential. Exploring high-risk insurance policies and driver monitoring programs can help drivers mitigate the effects of an accident on their insurance. Maintaining responsible driving behavior is paramount to improving driving records and reducing premiums over time.

Call to Action

If you have been in an accident, do not hesitate to seek comprehensive information about auto insurance options. Consult with insurance professionals to understand coverage limitations and explore solutions that meet your needs. Remember, auto insurance serves as a valuable financial safety net, ensuring protection against the unexpected.

{kind=link}