**Before the Introduction:**

Before delving into the complexities of auto insurance and multiple accidents, it is imperative to establish a comprehensive understanding of the subject matter. This article will provide a comprehensive overview of auto insurance, the implications of multiple accidents on coverage, and the options available for drivers with such histories. It will delve into the intricacies of policy terms, premium adjustments, and the role of insurance companies in managing risk. By providing a comprehensive analysis, this article aims to empower drivers with the knowledge to make informed decisions regarding their insurance coverage and financial protection in the event of multiple accidents.

Contents

- 1 Introduction

- 2 Understanding Multiple Accidents and Insurance Implications

- 3 Factors Influencing Premium Adjustments After Multiple Accidents

- 4 Coverage Options for Drivers with Multiple Accidents

- 5 Table: Auto Insurance for Multiple Accidents Coverage and Options

- 6 Strengths and Weaknesses of Auto Insurance for Multiple Accidents

- 7 FAQs on Auto Insurance for Multiple Accidents

Introduction

Navigating the complexities of auto insurance after multiple accidents requires a multifaceted understanding of coverage options and policy considerations. This introduction will provide a foundational overview of the potential consequences of multiple accidents, their impact on insurance premiums, and the importance of maintaining appropriate coverage levels. Furthermore, it will highlight the role of insurance companies in evaluating risk and the significance of driver safety and responsibility in mitigating insurance costs.

Following multiple accidents, drivers may face increased insurance premiums due to their perceived higher risk profile. Insurance companies assess risk based on factors such as driving history, accident frequency, and severity of claims. A history of multiple accidents can significantly impact these factors, leading to higher premiums as insurers seek to protect themselves from potential financial losses. Understanding the rationale behind premium adjustments can help drivers make informed decisions about their coverage options and driving behaviors.

Despite potential premium increases, maintaining adequate insurance coverage is crucial after multiple accidents. Insurance serves as a financial safety net, protecting drivers from the costs associated with property damage, bodily injuries, medical expenses, and legal liabilities. It is essential to carefully consider coverage levels and policy limits to ensure sufficient protection in the event of a future accident.

Insurance companies play a pivotal role in assessing risk and determining appropriate coverage levels for drivers with multiple accidents. They analyze driving records, accident reports, and other relevant information to establish a risk profile. Understanding the insurance company’s perspective can help drivers appreciate the factors that influence premium adjustments and coverage decisions.

Driver safety and responsibility are paramount in mitigating insurance costs after multiple accidents. Safe driving practices, such as adhering to speed limits, avoiding distractions, and maintaining vehicle maintenance, can help reduce the likelihood of accidents and demonstrate responsible driving behavior to insurance companies. By proactively addressing risk factors, drivers can potentially lower their premiums and improve their insurance eligibility.

Navigating auto insurance after multiple accidents can be challenging, but understanding the implications, coverage options, and insurance company perspectives is essential for making informed decisions about financial protection and driving safety. This article will provide a comprehensive exploration of these topics, empowering drivers with the knowledge and tools to effectively manage their insurance needs.

Understanding Multiple Accidents and Insurance Implications

Multiple accidents on a driving record can have profound consequences for auto insurance coverage and premiums. Understanding these implications and the associated insurance considerations is crucial for drivers seeking to maintain appropriate protection and manage costs.

When an accident occurs, insurance companies assess fault and liability to determine which party is responsible for the damages. In cases where the driver is found to be at fault, the accident will be recorded on their driving record, potentially leading to increased insurance premiums. Multiple accidents on a driving record can significantly impact premiums due to the perceived higher risk of future accidents.

Insurance companies use a variety of factors to calculate premiums, including driving history, age, location, and type of vehicle. A history of multiple accidents can raise insurance premiums as insurers seek to offset the potential for financial losses. It is important to note that the impact of multiple accidents on premiums can vary depending on the individual circumstances and insurance company.

In addition to premium adjustments, drivers with multiple accidents may face other insurance-related consequences. For example, they may be required to participate in a defensive driving course or install a monitoring device in their vehicle. These measures are intended to reduce risk and improve driving behavior, potentially leading to lower premiums in the future.

Understanding the implications of multiple accidents on insurance is essential for drivers seeking to maintain adequate coverage and manage costs. By carefully considering the potential consequences and taking proactive steps to improve driving safety, drivers can navigate the insurance landscape effectively and protect their financial interests.

Factors Influencing Premium Adjustments After Multiple Accidents

Following multiple accidents, insurance companies may adjust premiums to reflect the increased risk associated with the driver’s history. Several factors influence these premium adjustments, including the following:

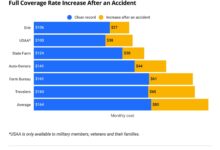

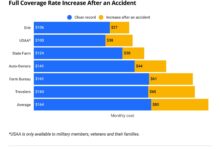

1. Number and Severity of Accidents: The number and severity of accidents on a driving record play a significant role in determining premium adjustments. Multiple accidents, particularly those involving significant property damage or injuries, can result in higher premiums due to the increased risk of future claims.

2. Fault Determination: Insurance companies assess fault and liability when determining premium adjustments. Drivers who are found to be at fault for multiple accidents will typically face higher premiums than those who are not at fault.

3. Time Between Accidents: The time elapsed between accidents can also impact premium adjustments. A recent history of multiple accidents within a short period of time may result in higher premiums than accidents that occurred further apart.

4. Driving History: Insurance companies consider the driver’s overall driving history when determining premium adjustments. A history of traffic violations, moving violations, or previous accidents can further increase premiums.

5. Age and Experience: Younger and less experienced drivers may face higher premiums after multiple accidents due to their perceived higher risk of future accidents.

Understanding the factors that influence premium adjustments is crucial for drivers seeking to manage their insurance costs. By addressing risk factors, such as improving driving behavior and avoiding accidents, drivers can potentially lower their premiums and improve their insurance eligibility.

Coverage Options for Drivers with Multiple Accidents

Despite potential premium increases, maintaining adequate insurance coverage is essential after multiple accidents. Insurance provides financial protection against the costs associated with property damage, bodily injuries, medical expenses, and legal liabilities. Drivers with multiple accidents should carefully consider the following coverage options:

1. Liability Coverage: Liability coverage is required by law and provides protection against damages caused to others in an accident. It covers bodily injuries, property damage, and legal defense costs.

2. Collision Coverage: Collision coverage provides protection for the driver’s own vehicle in the event of an accident, regardless of fault. It covers repairs or replacement of the vehicle.

3. Comprehensive Coverage: Comprehensive coverage provides protection against non-collision related damages, such as theft, vandalism, fire, and natural disasters. It covers the vehicle’s value, minus the deductible.

4. Uninsured/Underinsured Motorist Coverage: Uninsured/underinsured motorist coverage provides protection in the event of an accident with a driver who is uninsured or underinsured. It covers bodily injuries and property damage.

Drivers with multiple accidents should consult with their insurance agent to determine the appropriate coverage levels and policy limits for their individual needs. Maintaining adequate coverage is crucial for financial protection and peace of mind in the event of a future accident.

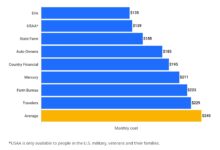

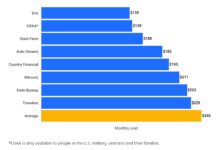

Table: Auto Insurance for Multiple Accidents Coverage and Options

| Coverage | Description | Key Considerations |

|—|—|—|

| Liability Coverage | Required by law; protects against damages caused to others in an accident | Coverage limits, exclusions |

| Collision Coverage | Protects the driver’s own vehicle in the event of an accident | Deductible, coverage limits |

| Comprehensive Coverage | Protects against non-collision related damages, such as theft, vandalism, and natural disasters | Deductible, coverage limits |

| Uninsured/Underinsured Motorist Coverage | Provides protection in the event of an accident with a driver who is uninsured or underinsured | Coverage limits, exclusions |

Strengths and Weaknesses of Auto Insurance for Multiple Accidents

Strengths:

1. Financial Protection: Auto insurance for multiple accidents provides financial protection against the costs associated with property damage, bodily injuries, medical expenses, and legal liabilities.

2. Peace of Mind: Knowing that you are financially protected in the event of an accident can provide peace of mind and reduce stress levels.

3. Legal Requirement: Liability coverage is required by law in most states, ensuring that you are meeting your legal obligations.

Weaknesses:

1. Premium Increases: Multiple accidents can lead to increased insurance premiums, potentially making it more expensive to maintain coverage.

2. Coverage Limitations: Insurance policies may have certain coverage limits and exclusions, which may not provide complete protection in all situations.

3. Potential for Denial or Cancellation: In some cases, insurance companies may deny or cancel coverage for drivers with multiple accidents, leaving them without protection.

Weighing the strengths and weaknesses of auto insurance for multiple accidents is crucial when making informed decisions about coverage options and financial protection.

FAQs on Auto Insurance for Multiple Accidents

1. What happens if I cause multiple accidents?

If you cause multiple accidents, your insurance company will evaluate the circumstances of each accident, determine fault, and adjust your premiums accordingly. Multiple accidents can lead to increased premiums due to the perceived higher risk of future claims.

2. Can I lower my insurance premiums after multiple accidents?

Potentially. By improving your driving behavior, taking defensive driving courses, and maintaining a clean driving record for an

{kind=link}