Contents

- 1 Navigating the Complexities of Post-Accident Insurance Changes

- 2 Introduction: The Aftermath of a Car Accident

- 3 Can I Switch Auto Insurance After An Accident?

- 4 Strengths and Weaknesses of Switching Auto Insurance After An Accident

- 5 Frequently Asked Questions (FAQs)

- 5.1 1. Can I switch auto insurance immediately after an accident?

- 5.2 2. Will my premiums increase if I switch after an accident?

- 5.3 3. Do I need to disclose the accident to my new insurer?

- 5.4 4. What if I have an outstanding claim with my current insurer?

- 5.5 5. Can I switch insurers if I’m at fault for the accident?

- 5.6 6. What is the best time to switch auto insurance after an accident?

- 5.7 7. Are there any fees or penalties for switching auto insurance after an accident?

- 5.8 8. What information do I need to provide when switching auto insurance after an accident?

- 5.9 9. Can I negotiate with my current insurer to reduce my premiums after an accident?

- 5.10 10. What if I decide not to switch auto insurance after an accident?

- 5.11 11. Is it possible to get coverage from a new insurer before I cancel my current policy?

- 5.12 12. What are my options if I can’t find affordable auto insurance after an accident?

- 5.13 13. Should I contact an insurance broker to help me switch auto insurance after an accident?

- 6 Conclusion: Making the Right Decision

- 7 Call to Action

- 8 Disclaimer

In the aftermath of a car accident, amidst the shock and disarray, one question that may linger in your mind is whether you can switch auto insurance providers. This article delves into the intricacies of this decision, exploring the factors to consider, potential consequences, and practical steps involved in changing insurers after an accident.

Introduction: The Aftermath of a Car Accident

A car accident can be a life-altering event, leaving both physical and emotional scars. In addition to the immediate aftermath, there are often long-term consequences to contend with, including potential insurance complications.

One common concern is the impact of an accident on your auto insurance policy. Will you face higher premiums? Will your coverage be affected? Can you switch insurers to secure a better deal?

In this comprehensive guide, we will provide answers to these pressing questions, offering guidance on the process of switching auto insurance after an accident.

Can I Switch Auto Insurance After An Accident?

In most cases, you can switch auto insurance after an accident. However, there are certain factors to consider and potential consequences to be aware of.

Factors to Consider:

1. Policy Terms: Review your current policy to determine if there are any restrictions or penalties for switching after an accident.

2. Timeliness: Some insurance companies may have specific time frames within which you must notify them of an accident.

3. Outstanding Claims: If you have any outstanding claims with your current insurer, it may be beneficial to wait until they are resolved before switching.

Strengths and Weaknesses of Switching Auto Insurance After An Accident

Strengths:

1. Potential Cost Savings: Comparing quotes from multiple insurers can potentially lead to significant cost savings.

2. Improved Coverage: New insurers may offer more comprehensive or specialized coverage options that better meet your needs.

3. Enhanced Customer Service: Switching to a different insurance company can provide you with access to better customer support and claims handling.

Weaknesses:

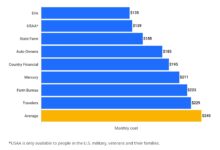

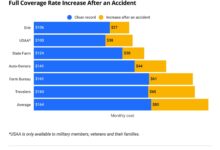

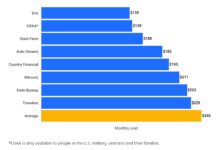

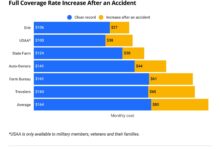

1. Premium Increases: In some cases, switching insurers after an accident can result in higher premiums.

2. Gaps in Coverage: If you do not switch insurers promptly, there may be a gap in your coverage, leaving you exposed to financial liability.

3. Claim Disputes: If you have an accident soon after switching insurers, there may be disputes over which company is responsible for the claim.

| Factor | Considerations |

|---|---|

| Policy Terms | Review policy restrictions and penalties for switching after an accident. |

| Timeliness | Note any deadlines for notifying your insurer of an accident. |

| Outstanding Claims | Consider waiting until outstanding claims are resolved before switching. |

| Potential Cost Savings | Compare quotes from different insurers to potentially save money. |

| Improved Coverage | Explore new insurers offering more comprehensive or specialized coverage options. |

| Enhanced Customer Service | Consider the quality of customer support and claims handling services of different insurers. |

| Premium Increases | Be aware that switching insurers after an accident may lead to higher premiums. |

| Gaps in Coverage | Avoid leaving a gap in your coverage by switching insurers promptly after an accident. |

| Claim Disputes | Consider potential disputes over claim responsibility if an accident occurs soon after switching insurers. |

Frequently Asked Questions (FAQs)

1. Can I switch auto insurance immediately after an accident?

In most cases, yes, but it’s advisable to check your policy and notify your insurer promptly.

It depends on the insurance company and your driving history. Some insurers may charge higher premiums after an accident.

3. Do I need to disclose the accident to my new insurer?

Yes, it’s crucial to disclose any accidents to potential new insurers to avoid coverage issues or claim denials.

4. What if I have an outstanding claim with my current insurer?

It’s recommended to wait until the claim is resolved before switching insurers to ensure a smooth transition of coverage.

5. Can I switch insurers if I’m at fault for the accident?

Yes, but be prepared for higher premiums or difficulty finding coverage from some insurers.

6. What is the best time to switch auto insurance after an accident?

Ideally, switch insurers promptly after the accident to avoid any gaps in coverage, but it’s also important to consider factors such as outstanding claims.

7. Are there any fees or penalties for switching auto insurance after an accident?

Some insurance companies may charge cancellation fees or impose penalties for early termination of your policy.

8. What information do I need to provide when switching auto insurance after an accident?

You will need to provide your driver’s license, vehicle information, accident details, and insurance history.

Yes, you can attempt to negotiate with your current insurer to lower your premiums, but the success of your efforts may depend on your driving history and the severity of the accident.

10. What if I decide not to switch auto insurance after an accident?

You can continue with your current insurer, but be aware that your premiums may increase and your coverage may not be as comprehensive as with other insurers.

11. Is it possible to get coverage from a new insurer before I cancel my current policy?

Yes, many insurance companies offer provisional coverage that will start on a specific date, allowing you to switch insurers without a gap in coverage.

12. What are my options if I can’t find affordable auto insurance after an accident?

You may consider exploring high-risk insurance companies, government-sponsored programs, or driver improvement courses to reduce your premiums.

13. Should I contact an insurance broker to help me switch auto insurance after an accident?

Yes, an insurance broker can assist you in comparing quotes from multiple insurers and finding the best coverage for your needs.

Conclusion: Making the Right Decision

Deciding whether to switch auto insurance after an accident is a complex decision that requires careful consideration of the factors discussed in this article.

While there are potential benefits to switching insurers, such as cost savings and improved coverage, there are also potential drawbacks to consider, such as premium increases and gaps in coverage.

By weighing the strengths and weaknesses, reviewing the FAQs, and consulting with insurance professionals, you can make an informed decision that best meets your individual needs and circumstances.

Call to Action

If you are considering switching auto insurance after an accident, take the following steps:

- Review your current policy to understand your options and potential penalties for switching.

- Get quotes from multiple insurance companies to compare rates and coverage.

- Disclose the accident to potential new insurers to avoid coverage issues.

- Consider working with an insurance broker to assist you in finding the best coverage for your needs.

- Make a decision that balances cost, coverage, and customer service to ensure you have adequate protection after an accident.

Disclaimer

Please note that the information provided in this article is intended for general guidance only and should not be relied upon as legal or financial advice. It is recommended that you consult with an insurance professional or attorney for personalized advice on your specific situation.

{kind=link}